The Philippines retirement income system has been ranked the fourth lowest of those reviewed by the 12th annual Mercer CFA Institute Global Pension Index, a study of 39 retirement income systems across the globe which covers almost two-thirds of the world’s population.

The 2020 Global Pension Index, which measures each retirement system through three sub-indices (sustainability, adequacy and integrity) includes two new systems – Belgium and Israel. This is the second year the Philippines, which is ranked 36th, has been included in the study.

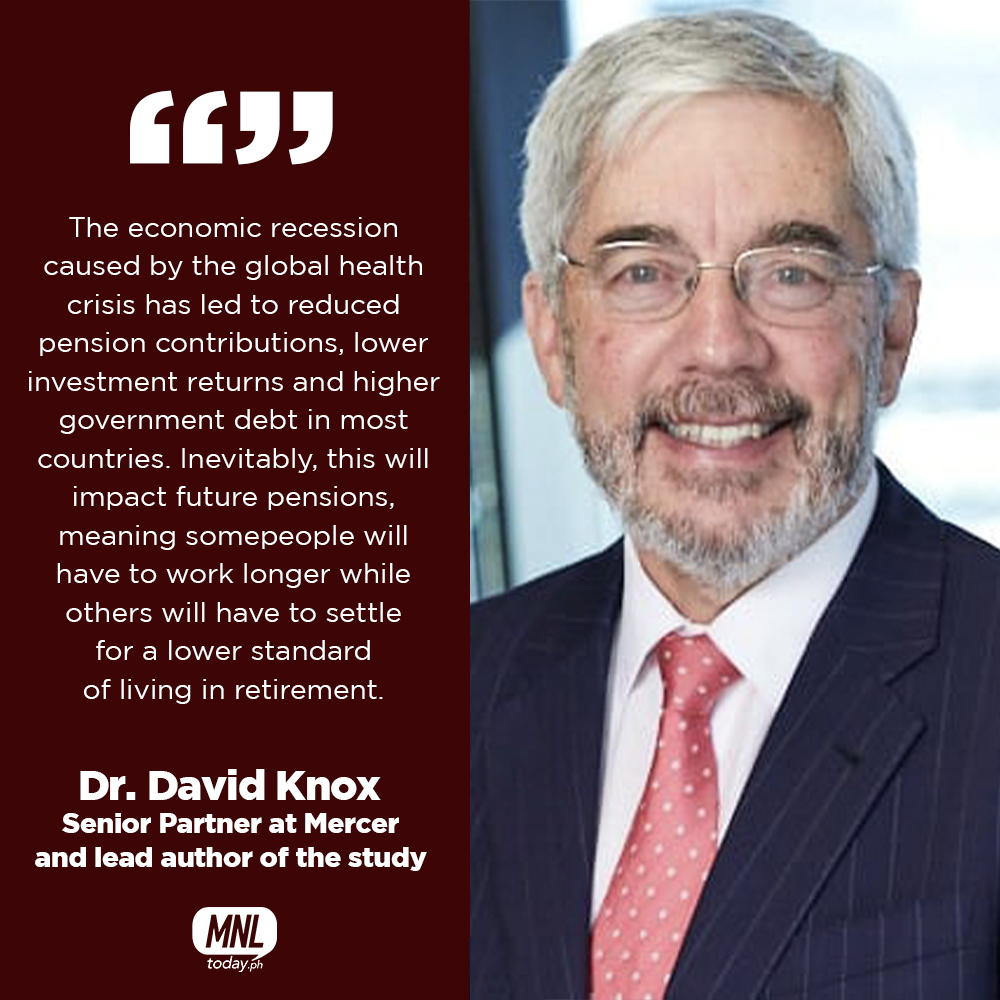

The Philippines’ overall index value decreased from 43.7 in 2019 to 43 in 2020, due to the study’s change in measure of life expectancy at the state pension age and not at birth, which more accurately reflects the period of retirement. For each sub-index, the Philippines scored highest for sustainability (53.4), followed by adequacy (38.9), and integrity (34.8).

The country is ranked 17th for sustainability, which measures the likelihood a system will be able to provide benefits into the future; 36th for adequacy, which looks at benefits, system design, levels of savings, and home ownership among others to determine a system’s ability to provide adequate retirement income; and 39th for integrity, which considers factors such as regulation, governance,

communication and operating costs.

Harold Tan, Mercer’s Wealth Business Leader for the Philippines said: “The overall index value for the Philippines system could be increased by raising the minimum level of support for the poorest elderly individuals along with broadening coverage of employees in occupational pension schemes. These

measures would work to grow the level of contributions and assets and permit the Philippines to set aside funds in the public system for the future, reducing reliance on the pay-as-you-go system. In order to preserve long term retirement savings, ‘no cash-out’ options must be introduced and put into place.”

The Philippines retained its “D” grade, connoting a pension system that has some desirable features, but also has major weaknesses and/or omissions that need to be addressed. The country is ranked in the same grade as a number of other Asian countries such as Japan, Thailand, China and India.

Meanwhile, the Netherlands had the highest index value (82.6) and has retained its top position and “A” grade in the overall rankings, notwithstanding the significant pension reforms occurring in that country. Thailand had the lowest index value (40.8).

For each sub-index, the highest scores were the Netherlands for adequacy (81.5), Denmark for sustainability (82.6) and Finland for integrity (93.5). The lowest scores were Mexico for adequacy (36.5), Italy for sustainability (18.8) and the Philippines for integrity (34.8).

Current Economic Environment Puts Additional Stress on Retirement Systems

The widespread economic impact of COVID-19 is heightening the financial pressures which retirees face, both now and in the future, the study found. Coupled with increasing life expectancies and the rising pressure on public resources to support the health and welfare of ageing populations, COVID-19 is

exacerbating retirement insecurity. The average sustainability score dropped by 1.2 in 2020 due to the negative economic growth experienced in most economies due to COVID-19.

“It is critical that governments reflect on the strengths and weaknesses of their systems to ensure better long-term outcomes for retirees.”

“Even before COVID-19, many public and private pension systems around the world were under increasing pressure to maintain benefits,” said Margaret Franklin, CFA, President and CEO at CFA Institute.

“We have learned a lot about the effectiveness of pension systems over the years, and while there is no single pension system model that will work for every country, the Global Pension Index provides comparative information to differentiate what is possible and practical in each market.”

COVID-19’s impact to the future of pension systems

The impact of COVID-19 is much broader than solely the health implications; there are long term economic effects impacting industries, interest rates, investment returns and community confidence in the future. As a result, the provision of adequate and sustainable retirement incomes over the longer term

has also changed.

The level of government debt has increased in many countries following COVID-19. This increased debt is likely to restrict the ability of future governments to support their older populations, either through pensions or through the provision of other services such as health or aged care.

To help alleviate the impact of COVID-19, governments deployed a diverse range of responses to support their citizens and pension systems.

Professor Deep Kapur, Director of the Monash Centre for Financial Studies (MCFS), said that many governments around the world have responded to COVID-19 with substantial fiscal stimulus, and central banks have adopted unconventional monetary policy. “The outlook for investment returns is muted while volatility may be elevated, adding to the normal challenges of risk management in a pension portfolio.

“Additionally, some governments have allowed temporary access to saved pensions or reduced the level of compulsory contribution rates to improve liquidity positions of households. These developments will likely have a material impact on the adequacy, sustainability and integrity of pension systems, thereby

influencing the evolution of the Global Pension Index in the coming years,” Kapur added.

The Philippines’ Government Service Insurance System (GSIS) set aside 43.01 billion pesos for a COVID-19 emergency loan program, of which 18 billion pesos has been disbursed to about 600,000 members and pensioners at the height of the lockdown. The program which allows members to borrow up to 40,000 pesos has been extended until December 27.

Mr Tan said: “While the government focuses on safeguarding the lives and livelihoods of businesses and its people, it should also keep in mind the longer-term impact associated with lockdowns and the related economic downturn which are affecting retirement savings. Coupled with market volatility and lower-for-longer interest rates, retirement security will come under greater pressure.”

COVID-19 has also increased gender inequality in pension provision.

Janet Li, Mercer’s Wealth Business Leader for Asia said: “Even before the pandemic, the genderretirement savings gap in Asia was exacerbated by the longer life expectancies of women, lower participation of women in the workforce and gender pay inequity. Now, that gap is expected to widen further, particularly in the hardest hit sectors where women represent more than half of the workforce, such as hospitality and food services.”

Photo Source: CTTO